Series: Cost of Living Crisis (Part 4 of 4)

Executive summary

Americans pay dramatically more for prescription drugs than other high-income countries. The reason is not that U.S. patients consume more medicine, or that the science is uniquely American.

The reason is structural: the U.S. built a market that rewards leverage over value. Patents can be extended, intermediaries can profit from opacity, and the biggest payer in the system historically could not negotiate.

This piece uses insulin as the clearest case study, then maps the broader machinery: patents and exclusivity, PBMs and rebates, Medicare rules, and the reforms that reliably lower prices.

I. Introduction: the insulin scandal

Americans ration insulin. Not because it is rare, and not because it is hard to make. Insulin is a century-old drug discovered in 1921, and modern versions are manufactured at scale by companies that sell the same products abroad for a fraction of the U.S. price.

It is worth pausing on the fact that drug pricing is not a frozen debate. In February 2026, CMS published updated materials for the Medicare Drug Price Negotiation Program, including an updated file for selected drugs and negotiated prices. That is the policy system, in real time, trying to turn “negotiation” from a slogan into an operating procedure.https://www.cms.gov/priorities/medicare-prescription-drug-affordability/overview/medicare-drug-price-negotiation-program/selected-drugs-negotiated-prices

That gap is the point. The story is not “insulin is expensive.” The story is that the United States has built a pharmaceutical market where monopoly protection, opaque intermediaries, and fragmented purchasing power allow prices to float far above what other high-income countries pay.

This article uses insulin as the most visible case study, then steps back to the broader system: patents, PBMs, Medicare’s historic inability to negotiate, and the policy levers that can lower prices while preserving real innovation.

II. The price gap, by the numbers

Charts

Medication blister packs (illustrative)

Image source: https://commons.wikimedia.org/wiki/File:Pills_in_blister_pack.jpg

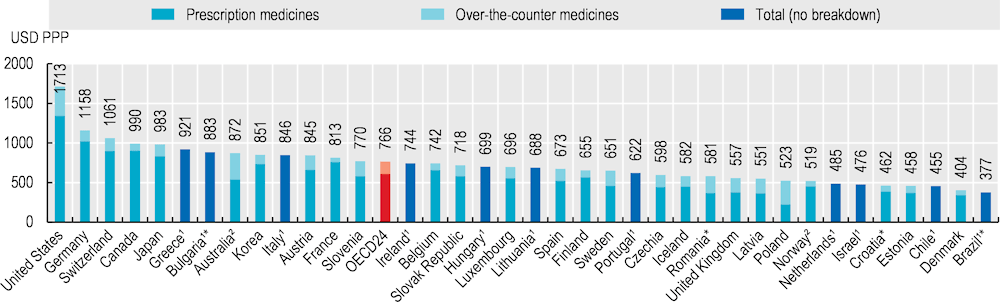

OECD benchmark: pharmaceutical expenditure per person

- Source: OECD, Health at a Glance 2025 (Pharmaceutical expenditure): https://www.oecd.org/en/publications/health-at-a-glance-2025_8f9e3f98-en/full-report/pharmaceutical-expenditure_ab82eef9.html#title-a20461ca91

OECD reports that per-capita expenditure on retail pharmaceuticals averaged USD 766 (PPP-adjusted) across OECD countries in 2023.

What to notice: even the OECD average is a large recurring household cost category, and the U.S. sits above most peers on multiple measures of drug spending and prices.

Medicare negotiation: selected drugs and negotiated prices (2026)

CMS publishes an official downloadable file (xlsx/csv) that can be charted (top negotiated drugs, distribution of 30-day prices, and similar).

Source: Selected Drugs and Negotiated Prices (CMS)

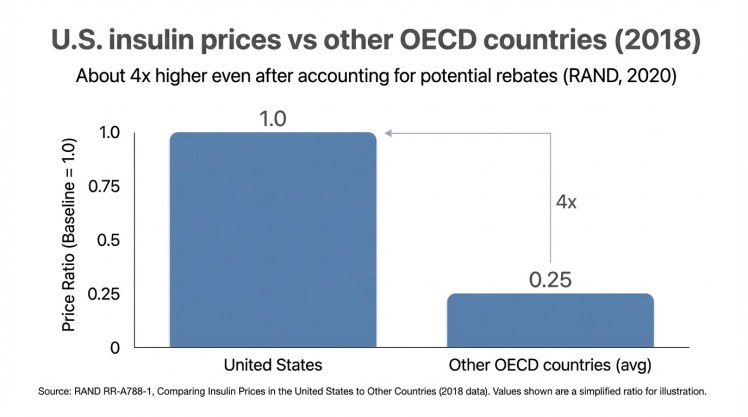

Insulin international comparison

Source: RAND — Comparing Insulin Prices in the United States to Other Countries (RR-A788-1)

Two facts can be true at once.

First, the U.S. leads the world in biomedical research, and Americans benefit from many breakthrough medicines.

Second, the U.S. pays far more for the same branded drugs than peer countries do, even when the drugs come from the same manufacturers.

The most consistent finding across cross-country studies is that brand-name prices drive the difference. Generics are often relatively inexpensive in the U.S. The outlier behavior is largely in patented medicines, where countries use negotiation and price-setting mechanisms and the U.S. historically relied on fragmented bargaining power.https://www.rand.org/pubs/research_reports/RRA788-1.html

What to notice: the gap shows up in aggregate spending, not just on a few headline drugs.

Sources

- RAND, International Prescription Drug Price Comparisons (Figure ES-1): https://www.rand.org/pubs/research_reports/RRA788-1.html

- OECD, Health at a Glance 2025 — Pharmaceutical expenditure: https://www.oecd.org/en/publications/health-at-a-glance-2025_8f9e3f98-en/full-report/pharmaceutical-expenditure_ab82eef9.html

What the data implies (in plain English)

When other countries pay less, it is rarely because they discovered a secret cheaper chemistry. It is because they use at least one of the following tools:

- A single buyer or coordinated buyers who can credibly say “no.”

- Formal negotiation backed by a reference price.

- Cost-effectiveness thresholds that set an acceptable price for public coverage.

In the U.S., by contrast, prices are often set in a way that rewards maximizing list price and then negotiating rebates through intermediaries that benefit from complexity.

That is why the harm shows up in real life. Patients delay or skip prescriptions. People ration drugs that are clinically dangerous to ration. Costs spill into medical debt and delayed care.

III. How did we get here?

What changed recently (2025–2026)

- Medicare negotiation became real policy, not just a talking point. CMS published Maximum Fair Prices for the first set of selected Part D drugs, with negotiated prices taking effect January 1, 2026.

- CMS: Selected drugs and negotiated prices (includes negotiated prices file): https://www.cms.gov/priorities/medicare-prescription-drug-affordability/overview/medicare-drug-price-negotiation-program/selected-drugs-negotiated-prices

- The Medicare drug benefit was redesigned to cap patient exposure. IRA changes phase in and culminate in an annual out-of-pocket cap for Part D, shifting costs away from patients with very high drug spending.

- Policymakers started targeting “middleman” structure directly. In January 2026, HHS issued guidance clarifying how manufacturers can offer direct-to-consumer lower prices with anti-kickback safeguards.

- A live open question: how big negotiated savings will be once statutory ceilings collide with existing rebates and net prices.

- Background analysis: https://pmc.ncbi.nlm.nih.gov/articles/PMC10397328/

The short version is that the U.S. created a pharmaceutical market with three reinforcing features:

- Long-lived market power that can be extended or protected from competition.

- A supply chain that rewards opacity rather than transparent price competition.

- Fragmented bargaining power for the groups that buy the most medicine.

Before getting into the mechanics, it is fair to steelman the case for the status quo.

- Patents are supposed to do a real job. A time-limited monopoly can make high-risk R&D financeable, especially for first-in-class therapies.

- Formulary management is not optional. Someone has to decide which drugs get preferred placement, and an intermediary can reduce administrative burden for employers and insurers.

- Blunt price ceilings can have costs. If policy ignores therapeutic value and uncertainty, it can reduce incentives to invest in high-risk areas or push launches toward the private market.

The problem is that the U.S. version of this system often turns those legitimate functions into open-ended leverage. Patents can be extended far past the intuitive “innovation window.” Rebates and spread pricing can reward higher list prices. And fragmentation means no single buyer can reliably say “no.”

That is why the reforms worth taking seriously are not “punish pharma” or “defend pharma.” They are reforms that preserve the reasons the system exists while removing the incentives to exploit it.

1) Medicare’s “noninterference” design (partially reversed)

When Medicare Part D was created in 2006, it was designed around private plans. The statute included a “noninterference” principle that limited the federal government’s ability to directly negotiate prices.

Private insurers and PBMs do negotiate, but their leverage is constrained. They can threaten to exclude a drug from a formulary, but for many blockbuster medicines the credible threat is weak because patients and physicians demand access.

The Inflation Reduction Act (IRA) changed the direction of travel by creating a negotiation pathway beginning with a limited set of high-spend drugs, then expanding over time.

2) Patents, exclusivities, and the art of extending them

Visual (WordPress-friendly): Patent lifecycle (typical)

| Phase | What happens |

|---|---|

| Discovery | R&D and early patents |

| Approval & launch | New drug enters market |

| Core exclusivity window | Prices stay high while competition is blocked |

| Secondary patents / device tweaks | Delivery, dosing, or formulation changes extend protection |

| Litigation / “thicket” | Competition delayed by legal risk and cost |

| Generic / biosimilar entry | Competition arrives, prices fall |

Patents are not inherently illegitimate. A time-limited monopoly can reward innovation.

The problem is that in practice, firms can stack and extend protections well beyond the “20 years from invention” mental model most people carry around.

Common strategies include:

- Evergreening: filing additional patents on delivery devices, dosing schedules, or minor formulation changes.

- Patent thickets: building dense clusters of overlapping patents that raise the legal cost and risk for biosimilar competitors.

- Pay-for-delay: agreements that postpone competition.

The result is predictable. Competition arrives late. Prices stay high longer than the science alone would justify.

3) PBMs and rebate-driven pricing

Visual (WordPress-friendly): Who pays whom (simplified)

- Manufacturer sets a list price.

- PBM negotiates rebates/fees with the manufacturer.

- Insurer or plan sponsor pays the PBM and sets coverage rules.

- Patient cost-sharing at the pharmacy counter is often tied to the list price, even when rebates reduce the plan’s net cost later.

PBMs sit between insurers, employers, pharmacies, and manufacturers. In theory, they can use scale to bargain lower prices.

It is also not hard to see why PBMs exist. A single employer generally cannot build the infrastructure to negotiate with thousands of pharmacies and manufacturers, adjudicate claims, and manage formularies. The “PBM as aggregator” is a reasonable concept.

But the problem is incentive design. In February 2026, federal PBM-related provisions were enacted that aim to delink PBM compensation in Medicare Part D from rebates and expand transparency and reporting requirements.https://www.kff.org/other-health/what-to-know-about-pharmacy-benefit-managers-pbms-and-federal-efforts-at-regulation/ Whether every detail works as intended, the direction is revealing: policymakers are increasingly treating opacity itself as a cost driver.

In practice, rebates can distort incentives. A PBM can appear to “save money” by negotiating a large rebate off a very high list price, while the underlying system still pays more than it would in a simpler, more transparent market.

That matters because many patients’ out-of-pocket costs are linked to list prices through deductibles and coinsurance. A large rebate paid later to a plan sponsor does not help a person who is paying at the pharmacy counter today.

4) Direct-to-consumer advertising and demand shaping

The U.S. (along with New Zealand) is unusual in permitting broad direct-to-consumer advertising for prescription drugs. Advertising does not create monopoly power, but it can reinforce it by steering attention toward branded, high-priced products and away from substitutes.

5) The “R&D cost” argument (and what it misses)

The industry argument is simple: high prices fund innovation.

Innovation does cost money, and drug development carries real risk. But the argument is incomplete without two additional facts:

- A large share of foundational research is publicly funded (for example, through the NIH and academic research systems).https://report.nih.gov/funding/categorical-spending

- High U.S. prices do not reliably map to proportionally higher innovation. Many countries with negotiation and price constraints still produce and adopt new medicines.https://www.oecd.org/health/health-at-a-glance/

A functioning policy goal is not “low prices at any cost.” It is prices that reward real therapeutic value without turning patents into a blank check.

IV. Insulin as a case study

Visual: how U.S. insulin prices compare internationally

Insulin syringe (illustrative)

Image source: https://commons.wikimedia.org/wiki/File:Insulin_syringe.jpg

Chart: U.S. vs other OECD countries

(See the RAND chart above in the “Price gap, by the numbers” section.)

Source for insulin price comparison

- RAND has a dedicated insulin comparison report with a clean summary and downloadable PDF: Comparing Insulin Prices in the United States to Other Countries (RAND, 2020)

What RAND found (using 2018 OECD data)

- Manufacturer prices in the U.S. were always higher than in the comparison countries they analyzed, often five to ten times higher.

- RAND notes that even after accounting for potential rebates, U.S. insulin prices would still likely be about four times higher than in other OECD countries.

Insulin is a near-perfect lens because it is both essential and old.

It is essential because people with Type 1 diabetes cannot substitute away. It is old because the underlying discovery is more than a century old.

A century-old discovery, modern pricing

Insulin was discovered in 1921. The famous telling is that the inventors sold the patent for a nominal amount so it could be widely available.

Yet U.S. insulin prices rose for decades and reached levels that forced rationing.

A concentrated market

Three companies dominate much of the U.S. insulin market: Eli Lilly, Novo Nordisk, and Sanofi.

A concentrated market is not automatically a conspiracy, but it is a setting where “shadow pricing” is easier and where competitive pressure is weaker.

Human consequences

When insulin is expensive, people do what rational humans do: they try to stretch it.

Unfortunately, insulin is not a drug you can safely stretch. Rationing can lead to emergency hospitalizations and death.

If you want a single moral test for whether a market is working, start here. A market where people ration a century-old, essential medicine because of price is not allocating resources efficiently.https://www.nejm.org/doi/full/10.1056/NEJMp1909402

What has changed, and what has not

Public pressure produced policy movement.

The IRA includes a $35 per month insulin cap for Medicare and created the pathway for broader Medicare negotiation.https://www.cms.gov/inflation-reduction-act-and-medicare Some manufacturers also expanded patient assistance programs.

Those steps matter. But they do not fully solve the problem for uninsured people and for patients whose out-of-pocket costs remain connected to list prices.

V. The innovation defense (and the actual tradeoff)

Any serious reform must confront a real tradeoff: if you push prices too low for genuinely breakthrough drugs, you can reduce incentives to invest.

But the current U.S. system often does something different. It allows firms to extract high prices even when additional value is modest, and it lets protections linger even after the core innovation has been recouped.

A better way to frame the question is:

- What prices and protections are warranted for high-value, first-in-class therapies?

- What should happen when a drug is old, widely used, and protected mainly by legal engineering?

Other countries answer this through explicit negotiation and cost-effectiveness frameworks. The U.S. has historically answered it through fragmented bargaining and administrative complexity.

Reform is about choosing a more deliberate answer.

VI. Policy solutions that actually lower prices

Visual: what reforms target which problem

| Problem | What it looks like | Policy lever (section) |

|---|---|---|

| Market power lasts too long | Patents/exclusivities extended beyond core innovation window | Patent & exclusivity reform |

| Prices set in the dark | List price ↑, rebates obscure net price | PBM transparency + incentives |

| Largest payer cannot set terms | Negotiation exists, but rollout is narrow/slow | Expand Medicare negotiation |

| Essential drugs still unaffordable | Patients ration; access depends on insurance status | Targeted tools: caps, importation, public manufacturing |

There is no single magic bill. A durable solution is a package that targets each layer of the system.

1) Expand Medicare negotiation (and speed up learning)

The IRA’s negotiation pathway is a structural shift. Once the largest payer can bargain, it changes the baseline expectations about “the market will bear it.”

The most reasonable critique is not that negotiation exists. It is that the initial rollout is narrow and slow relative to the scale of U.S. spending.

A practical direction is to widen the set of drugs subject to negotiation sooner, and to make the negotiation framework more responsive as evidence changes.

2) Use international reference pricing as a backstop

Reference pricing is not a perfect tool, but it is a simple one: anchor U.S. prices to a basket of peer-country prices.

As a backstop, it serves a purpose. If negotiation fails, the reference price creates a ceiling.

3) Patent and exclusivity reform

If you want lower prices without “punishing innovation,” start with the distinction between innovation and evergreen protection.

Policy options include:

- Tightening standards for secondary patents that provide limited clinical value.

- Speeding generic and biosimilar approvals.

- Increasing scrutiny of pay-for-delay agreements.

The goal is not to eliminate patents. It is to restore the expectation that competition arrives on time.

4) PBM transparency and incentives

PBM reform is about aligning incentives so lower prices flow through to patients.

The live policy debate is moving quickly here. Recent reporting describes reforms that shift PBM compensation toward administrative fees and require more rebate pass-through and transparency in Medicare Part D.https://www.ajmc.com/view/pbm-reforms-signed-into-law-reshaping-medicare-part-d-drug-pricing-transparency

Options include:

- Requiring clearer disclosure of rebate and spread pricing practices.

- Encouraging or requiring pass-through models in public programs.

- Reducing conflicts of interest when the same entity manages benefits and owns pharmacies.

5) Importation (useful, but not sufficient alone)

Importation from Canada is sometimes presented as a silver bullet.

It is not. Canada’s market is not large enough to supply the U.S., and Canada has its own incentives to restrict exports.

But as a targeted tool, it can create competitive pressure and provide relief for specific medicines.

6) A public manufacturing option for essential generics

In markets where competition fails and a drug is essential, a public manufacturing option can function as a price ceiling.

This does not need to become a full government takeover of pharma. It can be a narrow tool for drugs with chronic market failures.

7) Reduce the role of direct-to-consumer advertising

Limiting direct-to-consumer advertising would not solve pricing on its own, but it would reduce one force that supports high list prices by manufacturing demand for branded products.

VII. What other countries do differently

Other high-income countries vary in details, but most share a common feature: they do not treat the list price as the “starting point” that must be accepted. They treat it as an opening bid.

Germany

Germany negotiates prices through health funds and uses reference pricing when agreement fails. Access is broad, and Germany still supports a strong pharmaceutical sector.

United Kingdom

The U.K. uses cost-effectiveness analysis. If a manufacturer wants public coverage, it must offer a price that meets the system’s threshold.

Canada

Canadian provinces negotiate collectively and use reference pricing practices that keep prices closer to peer norms.

The key lesson

These systems are not anti-innovation. They are anti-blank-check. They separate “pay more for real breakthroughs” from “pay more because the paperwork is engineered to keep competition out.”

VIII. What will not work

Some ideas sound appealing but fail in practice.

- Voluntary industry promises. They can change with leadership, market conditions, or public attention.

- Copay cards. They mask prices rather than fixing them, and can raise total system spending.

- Importation alone. Scale constraints make it insufficient.

- Waiting for competition in already-concentrated markets. When entry is blocked by patents and thickets, “the market” will not self-correct on schedule.

IX. Conclusion: affordable drugs are possible

Lower drug prices are not a war on innovation. They are a demand for a market that works.

The U.S. model is not uniquely innovative. It is uniquely permissive. It allows monopoly protections to be extended, hides true net prices behind rebate games, and splinters purchasing power so that the largest payer historically could not negotiate.

A practical package looks like this:

- Expand Medicare negotiation faster and more broadly than the initial IRA rollout.

- Use international reference pricing as a backstop when negotiation fails.

- Reform patents and exclusivities to limit evergreening and reduce pay-for-delay incentives.

- Regulate PBMs for transparency and pass-through so savings flow to patients and payers.

- Target essential drugs with persistent failures using tools like importation and public manufacturing.

Insulin shows what happens when policy tolerates extraction in a market where people cannot walk away. The fix is not a single magic bill. It is a set of rules that forces the market to compete on value rather than on leverage.

Sources and further reading

This article draws on the following primary and high-quality secondary sources.

- RAND: Comparing Insulin Prices in the United States to Other Countries (2018 data; published 2020).https://www.rand.org/pubs/research_reports/RRA788-1.html

- RAND: International prescription drug price comparisons (context on broader brand vs generic differences).https://www.rand.org/pubs/research_reports/RRA788-1.html

- CMS: Medicare Drug Price Negotiation (Inflation Reduction Act). https://www.cms.gov/inflation-reduction-act-and-medicare/medicare-drug-price-negotiation

- OECD — Health at a Glance 2025, “Pharmaceutical expenditure”. https://www.oecd.org/en/publications/health-at-a-glance-2025_8f9e3f98-en/full-report/pharmaceutical-expenditure_ab82eef9.html#title-a20461ca91

- NIH: categorical and overall spending (for context on public research funding). https://report.nih.gov/funding/categorical-spending

- NEJM perspective on insulin affordability and access (background on rationing harms). https://www.nejm.org/doi/full/10.1056/NEJMp1909402

- OECD: Health at a Glance (international health system and spending comparisons). https://www.oecd.org/health/health-at-a-glance/

{kind=link}

{kind=link}